We entered the quarter in the throes of an unexpected conflict between the US, Israel and Iran, with both bond and equity markets moving in lockstep with the oil price: the most visible barometer of the potential disruption to the global economy.

Quickly, though, the market regained its footing, placing increased weight on President Trump’s assurances that the conflict would be resolved soon. In late June, the promised deal had been struck between the US and Iranian officials. The 14-point Memorandum of Understanding included an “immediate and permanent termination of military operations on all fronts”. Compliance with the deal’s terms has been patchy, but at the time of writing there appears to be a willingness on both sides to make it work in some form. Despite this turbulence, global equities notched a gain of 14% in the quarter. In what follows, we discuss some of the lasting impacts of the conflict, before delving into the factors that have driven equities higher.

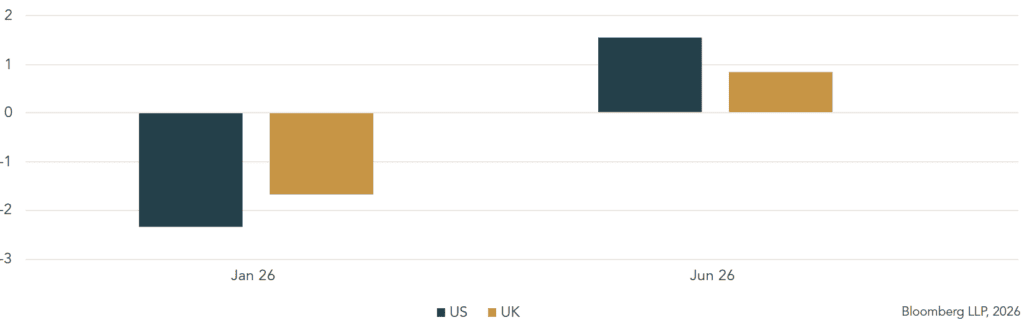

Putting aside the geopolitical ramifications of the conflict, which will no doubt be significant, the cessation of hostilities has not stopped the war from leaving a lasting economic impact. As the oil price spiked in response to the closure of the Strait of Hormuz, bond yields rose rapidly to reflect the inflationary impact. Oil has since fallen from $118 to $73 at the end of the quarter, but the legacy of the war continues to linger in bond markets. For example, we started the year with markets pricing several implied rate cuts by central banks in the US and UK. Both the Bank of England and the Federal Reserve are now expected to hike rates before the year is over. This reversal in policy direction was bolstered by the arrival of Trump appointee Kevin Warsh as Chair of the Federal Reserve, who surprised markets with some relatively hawkish rhetoric on inflation. Forecasts for near term inflation have remained elevated despite the recent drop in the oil price, reflecting some inflationary pressure embedded in other areas.

Number of Hikes/Cuts to Central Bank Policy Rate Expected in 2026

This environment has implications for the types of assets and sectors that are likely to outperform and we are pleased to have meaningful exposure to real assets in our portfolios in this context.

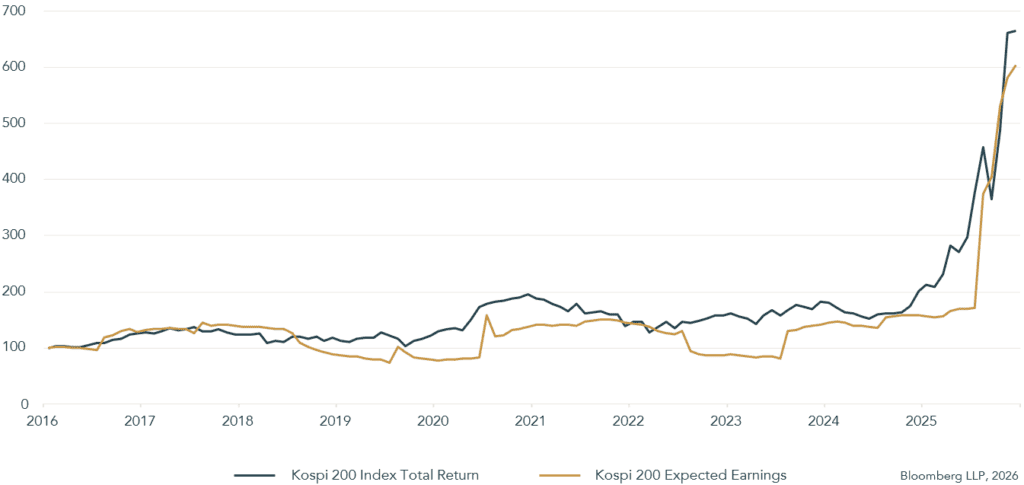

One reason for the equity market’s optimism has been rapid earnings growth, particularly from companies tied to the boom in Artificial Intelligence (AI). We wrote in February that the best balance of risk and reward in the AI supply chain looked to be in the hardware suppliers, particularly those in South Korea and Taiwan. The unique position of Asian technology markets to harvest the profits from the immense capital expenditures by leading model developers has led to exceptional returns from the region’s equity markets this year. South Korea’s Kospi 200 index, which tracks the country’s largest equities, has returned 127% so far this year, whilst Taiwan’s main index has risen 62%. Even more remarkably, most of the gains in these indices, both this year and last, have been driven by phenomenal earnings growth by constituent companies. This growth in earnings, which is shown for the South Korean market below, means that by conventional valuation metrics, such as price-to-earnings ratios, these shares do not look particularly expensive.

However, the build-out of AI infrastructure is not conventional in many ways. The amount being spent on capital expenditure by the industry’s ‘hyperscalers’, predominantly US tech companies, is virtually unprecedented. The size of the prize for those who can secure a dominant market position in the delivery of AI to the world economy is equally vast. With some exceptionally profitable US companies building expensive infrastructure which they see as essential to their survival, the shortages in component parts, such as high bandwidth memory, are expected to persist for some time. We share this expectation but are also mindful that supernormal profits tend to be competed away, if not by competitors, then by ill-discipline on the part of existing suppliers. There is also the risk that technological progress will temper the red-hot demand for certain inputs as chip designs are optimised for cost efficiency. With some pockets of exuberance now evident in markets connected to these linchpins in the AI supply chain, we have trimmed our exposure to this area recently, notwithstanding the fact that these companies will likely continue to see supernormal earnings for some time.

South Korean Equity Market Returns

Such has been the influence of geopolitics and AI on markets that the resignation of Prime Minister Starmer in late June was barely registered by the global investment community. Sterling, gilts and UK equities gave a very muted reaction to the announcement, in part because it had started to look inevitable, with bond markets having already moved to reflect the perceived impact of a UK government under his likely successor, Andy Burnham. Whilst Burnham has committed publicly to operating within the existing fiscal framework, UK gilt yields have risen as the bond market anticipates more borrowing from the UK government. It is too early to say whether or not the change of leadership will materially affect the direction of travel for UK assets. It is important to remember when drawing conclusions between UK politics and its stock market that over 75% of the earnings of FTSE 100 companies come from overseas. Even the FTSE 250, which tracks the next 250 largest companies, generates over 50% of its revenues from overseas. As a result, any material impact on UK equities is likely to be company or sector specific.

As we move through the year, domestic politics in the US is likely to come into sharper focus. Prediction markets currently suggest that the Democrats are likely to regain the House of Representatives at the midterm elections in November and may also gain seats in the Senate. If this weakening of the Republicans’ grip on the legislature were to happen, this would likely have implications for policy as well as the actions of President Trump. The areas most affected will be those requiring new legislation (as opposed to those carried out by executive action). Likely targets would be tariffs, cuts to healthcare spending, immigration enforcement and cryptocurrency legislation. The House alone cannot force a repeal of Trump’s policies, meaning that blocks and delays are most likely, which is likely to curtail the Trump administration’s fiscal freedom somewhat. More generally, we will likely see a waning of the President’s influence on global affairs as is often the case towards the end of a second term.

It feels cliché to conclude that we expect volatility in many of the markets we invest in to continue, but it is nonetheless our expectation. Focusing on long-term trends and placing more weight on data than on news is more important today than ever. In doing so, we believe we have curated a portfolio of exciting and durable themes that are fit for the rapid pace of change, both technological and political, which we see in the world today.

Fred Hervey

Chief Investment Officer