“Every act of energy conservation… is more than just common sense: I tell you it is an act of patriotism.”

Jimmy Carter, former US President, during the energy crisis of 1978–79

South America finds itself on the cusp of a revolution, emerging, as it periodically does, as one of the more interesting corners of the global equity market. Politics across a number of countries has shifted in a more market friendly direction, real interest rates remain positive with room to be cut, and local equity markets are geared to energy and commodities at a time when the world is rediscovering the value of secure supply. Despite this, the region remains a negligible part of global equity benchmarks. In a world where energy security and geopolitics are central to the macroeconomic narrative, South America’s combination of political change, financial discipline and resource endowment deserves closer inspection.

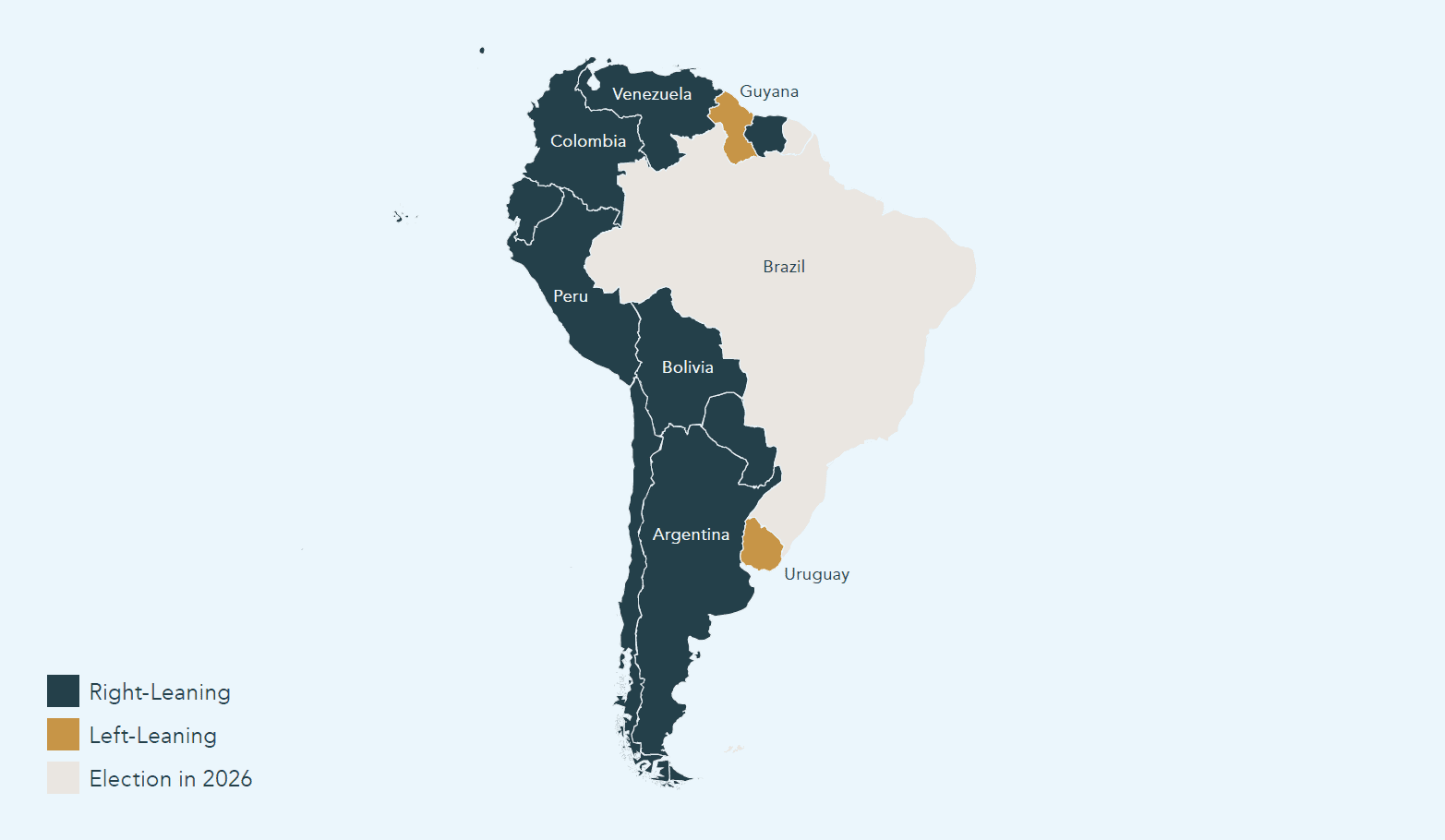

The political backdrop looks very different to the “pink tide” narrative that has framed investor perceptions for much of the past two decades, where left-of-centre governments swept to power in South, and indeed, Latin America in the early 2000s. Across 2025, right-of-centre or explicitly pro-market candidates won presidential races in countries such as Argentina, Chile, Ecuador and Bolivia, while a conservative victory in Costa Rica early in 2026 extended this into Central America. These results reflect public frustrations with crime, excessive inflation and weak growth, and the electoral map that has emerged is notably more market-friendly than in the 2000s and 2010s. New administrations are generally talking about smaller and more focused states, deregulation in sectors such as energy and mining, and the need to attract foreign direct investment. Although social demands remain high, and most governments must balance the interests of Washington, Beijing and domestic pressures, the economic regime has undoubtedly shifted rightwards, with economic liberalisation high on the agenda. The pattern is not without exception, with Brazil increasingly likely to re-elect leftist leader Luiz Inácio Lula da Silva later this year, but the tide has turned in favour of right-of-centre parties across the continent.

Argentina is the clearest expression of this free-market turn. President Javier Milei’s administration has set out to deliver what he calls “shock therapy”, combining a brutal fiscal adjustment with an ambitious liberalisation programme. The government has moved to deregulate trade and services, unwind rent and price controls, open sectors such as energy, transport and healthcare to greater competition, and prepare state owned enterprises for eventual privatisation. The policy changes have required expending significant social and political capital, with Milei nearly displaced in recent elections thanks to his radical actions, but early results from the platform of liberalisation are quite striking. The fiscal deficit has swung into surplus, and inflation has fallen sharply from peak levels. This pattern, albeit likely to a lesser degree, may be implemented across South American states as their governments move rightwards. If these countries can follow Argentina’s lead, then the benefits are clear: Argentina’s stock market has rallied over 340% since Milei won the 2023 election.

Political Landscape in South America

Monetary policy distinguishes South America just as clearly. Having learnt their lessons in previous crises, many central banks in the region moved earlier and more forcefully than their developed market counterparts when inflation accelerated in 2021. Policy rates were taken to levels that left real yields – the yield on bonds after accounting for inflation – firmly positive. Brazil reached a real yield of over 11% recently, while Colombia, Bolivia, and Mexico all recorded levels in the high single digits. Although those numbers partly reflect idiosyncratic credit and inflation dynamics, they also underline how far the region went to rebuild credibility after earlier cycles of inflation and devaluation. For context, real yields in the United States have fallen to -1%.

That early and aggressive tightening has begun to bear fruit. Several South American economies saw inflation peak earlier and fall faster than in advanced economies, precisely because policy moved pre emptively. In countries like Brazil and Chile, policy rates have already started to move lower from very restrictive levels, yet real yields remain among the highest in the investable universe, leaving scope for further cuts if inflation expectations can remain anchored. For investors, visible room for an easing cycle is fundamentally beneficial and typically supportive of domestic demand, banking system profitability and equity valuations, helping to create a virtuous cycle of growth.

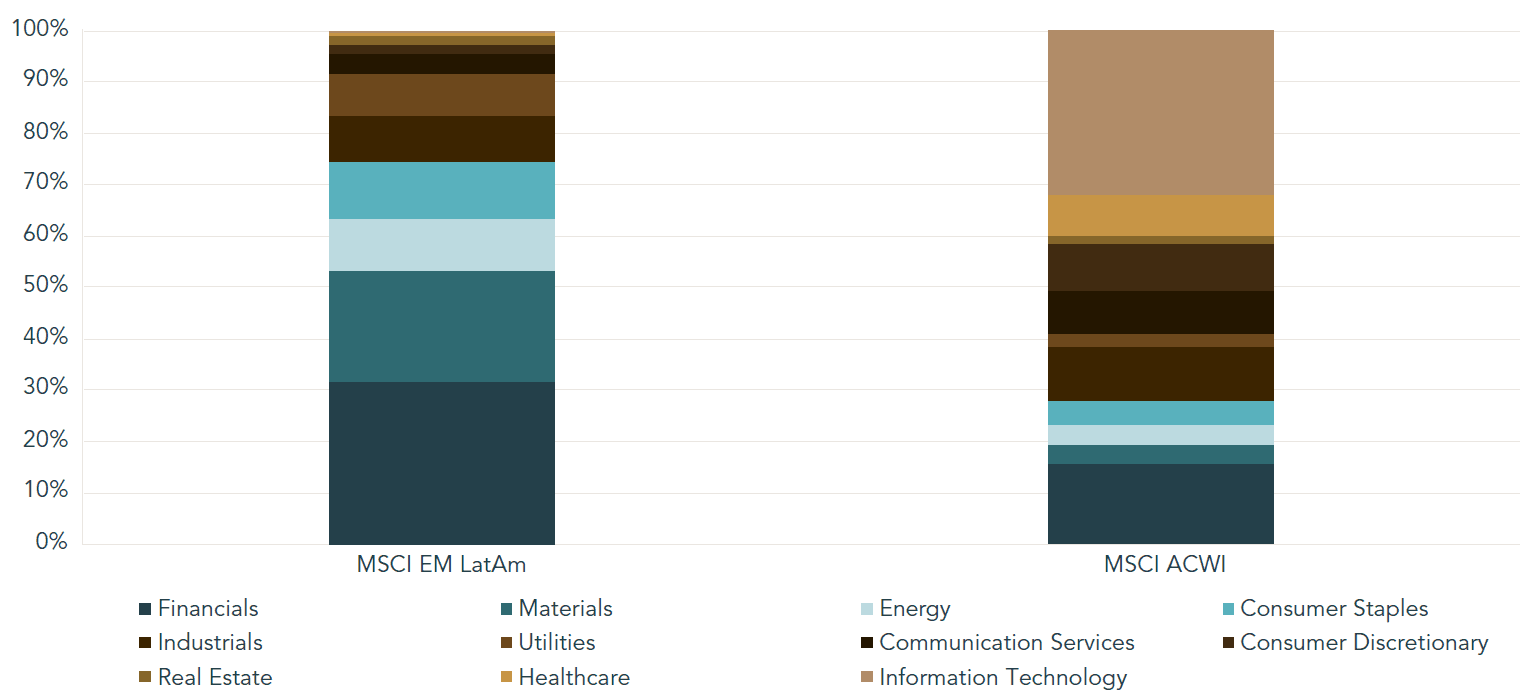

At the equity index level, South America also looks very different to the parts of the market that have led over the last decade. The MSCI EM Latin America universe is dominated by financials, materials and energy, with financials at roughly a third of index weight, materials close to a fifth and energy above 10%. These sectors are natural beneficiaries when growth is supported by higher commodity prices and improving fiscal positions. This sits in sharp contrast to the global benchmark MSCI All Country World Index, where information technology alone accounts for over 30% of index weight, and energy and materials are only 7% between them.

MSCI EM Latin America vs MSCI All Country World Index Sector Composition

Furthermore, within the global benchmark, Latin America barely registers, with the region’s aggregate share of global equity indices below 1%, despite representing over 6% of global GDP. The result of this is that South America (as part of Latin America) is structurally under owned, yet geared to commodity prices and the re-shoring thematic, in which countries are looking to re-domicile production of key industries. This re-emergence of asset-heavy investment stands in contrast to the global asset-light equity trade that has dominated in recent years, thanks to a combination of low interest rates and fiscal largesse. If the macro regime is shifting towards more volatile geopolitics, which we believe it is, then we would expect Latin America to grow as a proportion of the world index thanks to this attractive sector composition.

Just as Argentina has benefitted from more liberal politics and implicit American support, Venezuela may be in line for similar tailwinds. Nowhere is the disconnect between resource endowment, economic potential and benchmark representation starker. From 2017 onwards, Washington imposed sweeping sanctions on the leftwing populist Maduro regime and state oil company PDVSA, effectively halting Venezuelan crude exports to the US and depriving the state of its main source of dollar-based income. The aim was openly political: to force a move back toward free and fair elections and to signal that authoritarian rule would carry large economic costs.

For bondholders, the consequences were immediate and severe. Venezuela and PDVSA, the state oil company, fell into default in late 2017, and roughly $100 billion of bonds have since traded at distressed levels, with market activity further constrained by a US ban on dealing in the debt from 2018 to 2023. The sovereign bond’s exclusion from key fixed income benchmarks furthered the process of financial isolation as natural owners were forced to sell.

Since then, the bonds have rallied on a roster of more positive news, as an auction of secured assets gave certainty to PDVSA bondholders, while the increasing likelihood of a debt restructuring thanks to US pressure benefitted the sovereign bonds. This process was accelerated when the US extracted Maduro from the country in a regime change reminiscent of the 1970s.

The country’s debt began to reflect the fact that America’s involvement in the country would bring with it increased foreign direct investment that could well rejuvenate a once wealthy country, and indeed the recently announced debt restructuring is the first step towards that. The Iran War only accelerated the strategic importance of Venezuela’s oil reserves, and made clear the US’s desire for dominion over the western hemisphere, including Venezuela.

Despite Venezuela’s future importance in global energy markets, the more immediate driver in 2026 has been the escalation of conflict in the Middle East. War in the region, attacks on oil and gas infrastructure, and a blockade of the Strait of Hormuz have resulted in significantly increased energy costs. Around 25% of global seaborne oil and 20% of liquid natural gas travelled through the Strait before the war. Attacks on oil tankers and competition for control of the Strait has reduced flow meaningfully, injecting a geopolitical risk premium into both oil and gas prices.

So far, the result is a volatile market for energy, especially as negotiations flip-flop between the US and Iran, with Brent Crude prices at one point rising above $120 per barrel, while gas prices also spiked. In this environment, divergence has begun to open up between countries that are energy importers and those that are energy exporters. Outside of the Middle East, exporters, including those in South America, are natural beneficiaries of both higher realised prices and renewed attention to supply diversification and contractual security. Conversely, those reliant on energy imports, such as the ASEAN region, will likely suffer from the higher costs of energy products.

A clear indicator of the speed at which global oil supply can and has shifted is the United States, where oil exports are 2m barrels a day higher than at the same time last year. The shift in South America’s own energy balance should follow suit, although perhaps at a slower pace. Prior to the conflict, Brazil had already seen crude overtake soybeans as its largest export, while Colombia and Guyana also run positive oil trade balances. Over time, Venezuela is expected to return production back toward the 3m barrel output level it previously operated at, as international energy flows reroute along new geopolitical lines. The region’s share of global output remains modest, but for these economies higher energy prices now improve the terms of trade and can support both fiscal revenues and local currencies.

This backdrop leaves South America in a relatively unusual position. The increasing importance of a secure, diversified supply of energy, a sectoral makeup that is increasingly attractive in a world where real assets are valued more highly than before, and central bank policy that provides room for economic stimulus all coalesce around the same collection of countries. Taken together, the outlook for South America has rarely looked better.

Lincoln Private Investment Office.

This document has been prepared and distributed for information by Lincoln Private Investment Office LLP (“LPIO”) and is a marketing communication. LPIO is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute an offer by LPIO to enter into a contract/ agreement, nor is it a solicitation to buy or sell any investment. Nothing in this document should be deemed to constitute the provision of financial, investment or other professional advice in any way.