The first quarter of the year proved a tale of two halves. Through January and February, markets continued where they had left off in 2025. Buoyed by the prospect of interest rate cuts and stimulative fiscal policy in developed markets, cyclical regions and sectors performed well, whilst beneficiaries of progress in the AI ecosystem also posted strong gains.

When the US and Israel launched strikes on Iran on 28th February, a spike in the price of energy put many of these trends into reverse. We take this opportunity to explain how we are thinking about these events, as well as discussing some structural forces which we believe will be enduring investment themes.

At the end of February, equities had enjoyed a robust start to the year. Whilst the US market was broadly flat over this period, major non-US markets were generally higher, with the FTSE 100 a particular highlight, having gained 10% in two months. South Korea was a clear standout in Asia, with several of its largest companies benefitting from the vast sums being spent by US technology companies on the hardware underpinning artificial intelligence. Supported by renewed weakness in the US dollar and resilient global growth, commodities also started the year strongly, with the Bloomberg Commodity Index adding 12% to the end of February. Oil, which would go on to become the headline commodity of the quarter, had also been rising steadily since the start of the year.

Much has been written about the conflict in Iran. Conscious that the speed of change means any direct commentary may become quickly outdated, we will focus on the big picture economic impact of the initial events. Within a few days of the conflict breaking out, Iran closed the Strait of Hormuz, a vital artery of global trade which, amongst other things, carries c.20% of global oil and gas supply, a third of global fertilizer supply and a significant proportion of other industrial inputs such as aluminium and helium. The prices of these commodities have shot up, for example crude oil rose 95% in the quarter to finish March at $119 per barrel. Equities and bonds were rattled by the shock, with global equities down over 6% in March and regions with a greater reliance on Middle Eastern oil, like Japan and India, falling over 10%. Government bonds, traditionally a safe haven in times of crisis, offered little protection as markets drew the connection between higher oil prices and inflation, resulting in higher yields (and lower prices).

As the war continued, the nuances of the economic impact started to seep into asset values. Bond yields, for example, retreated from their highs as the market began to consider the fact that the inflation impact could be one-off, whilst the growth headwind from energy prices eating into consumer and corporate budgets could be more sustained.

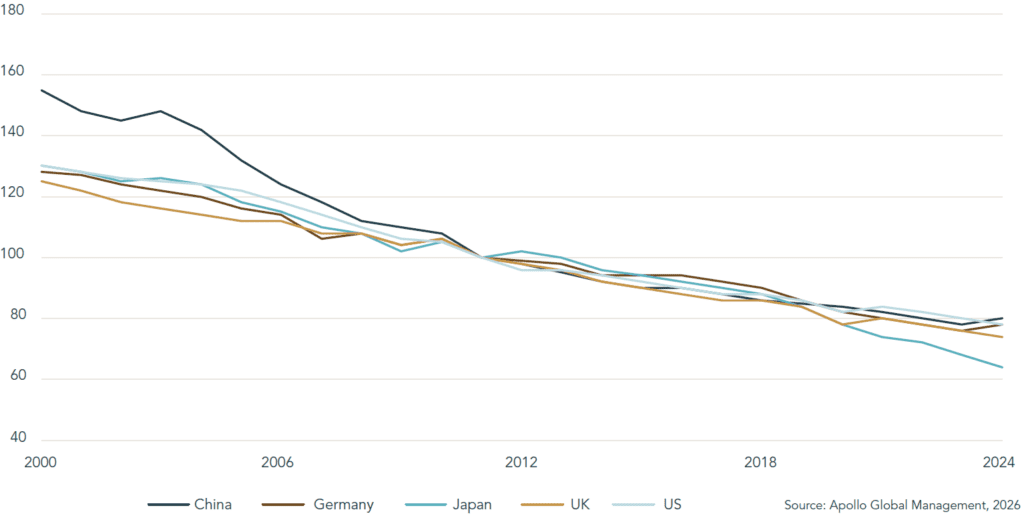

Oil Intensity of GDP (Indexed to 100 at 2011)

The scale of this growth impact is the subject of much debate. Historically, oil spikes of this magnitude have spelled trouble for the global economy. However, there are some mitigating factors in today’s situation. Not least, the chart above, which shows that major global economies are much less energy intensive than they used to be, which means they should be in a better position to cope with disruptions in energy supply. That is not to dismiss the potential impact by any means, but it limits the usefulness of historic parallels such as the Yom Kippur War (1973) or the Gulf War (1990–1991).

Economists at Apollo Global Management have adapted the Federal Reserve’s economic models to show that a sustained move in oil to $100 would reduce US GDP growth by a cumulative 0.1% over a few quarters. Such analysis is of limited use while the range of outcomes in Iran remains wide. Oil could conceivably fall significantly in the event of a detente, whilst any escalation could see prices rise materially above $100, although if accompanied by a forced opening of the Strait by military means, this may help to contain oil prices. On the flipside, even if we were to see a sustainable ceasefire, the damage already done to energy infrastructure across the Middle East may leave a lasting impact on energy prices as these facilities take time to rebuild and restart. Moreover, we may see a period of elevated demand for oil and other commodities as governments stockpile reserves to insure themselves against a repeat event in future.

In times like these, it is valuable to remember that we invest for the long term. This liberates us and our managers from attempting to second guess diplomatic developments between nations at war and focuses our minds on the longer-term direction of economies and markets. In this regard, it is notable that inflation expectations reflected in bond market pricing remain relatively well-anchored for the coming years. Of course, this may change, particularly if the conflict goes on for longer than the 2-3 further weeks President Trump had indicated at the time of writing. The volatility of March will no doubt persist for a while longer.

Whilst volatility in and of itself is not desirable, and indeed we seek to mitigate some of its impact through uncorrelated positions in our portfolios, large price fluctuations in individual equities or sectors create opportunities. Indeed, in several instances our managers have added to positions where the market has misunderstood the impact of a spike in energy costs on the intrinsic value of a business.

There were bouts of volatility earlier in the quarter too, this time caused by worries about the disruptive potential of AI. Among the sectors most severely affected was software, with AI’s power to automate the provision of certain services leading the market to re-evaluate the viability of software-as-a-service business models or the pricing power that such companies might have. We have relatively modest levels of exposure to the sector, with many companies starting the year trading at valuations that offered a limited margin of safety. We are now starting to see some of our active managers begin to capitalise on mis-pricings in certain software companies that have entrenched business models which are difficult to disrupt. Interestingly, speaking to our private equity fund managers who are deeply involved in the operations of their portfolio companies, including some in software, we hear that in many cases AI is enhancing the breadth and quality of service offered to clients. We expect this bifurcation to continue between deeply entrenched businesses delivering a critical service and those in a weaker competitive position, creating opportunities for expert investors in the sector.

A relative bright spot this quarter has been our position in UK smaller companies. Small cap equities trade at a meaningful discount to large caps in most major markets across the world. With UK equities as a whole among the cheapest in developed markets, UK small cap must surely be up there with the least popular asset classes in the world. Defying the performance of the sector, which gave up its good start to the year in the turmoil of March, our position in UK small caps returned 11% in the quarter. This demonstrates both the quality and growth potential available in smaller companies, as well as the valuable role active fund management plays in less efficient markets. We believe the story has room to run considerably further.

Seeing fundamental forces play through like this is a valuable reminder in volatile times. Through the headlines and market moves, there will be opportunity as well as heightened risks. These are also moments when our partnerships with highly skilled fund managers come to the fore, as it is often they who capitalise on this volatility on our behalf, as well as managing changing risks. By mixing these actively managed strategies with passive instruments, our portfolios are constructed to be nimble – a valuable characteristic when information is changing quickly. However, as long-term investors, this capability to move quickly does not necessarily mean we set out with the intention to do so.

Fred Hervey

Chief Investment Officer